Founder | BPI® Energy Auditor Certified Professional

Courtesy of The Philadelphia Inquirer; Image Source The Urban Institute

When the average age of baby boomers was 35, in 1990, the value of the homes they owned was close to a third of the entire U.S. housing market.

For Generation X, it was 20 percent, or one fifth, in 2008.

Millennials haven’t reached 35 as an average age yet, but at 31 and owning 4 percent (less than one-twentieth!), they aren’t on track to come anywhere close to previous generations.

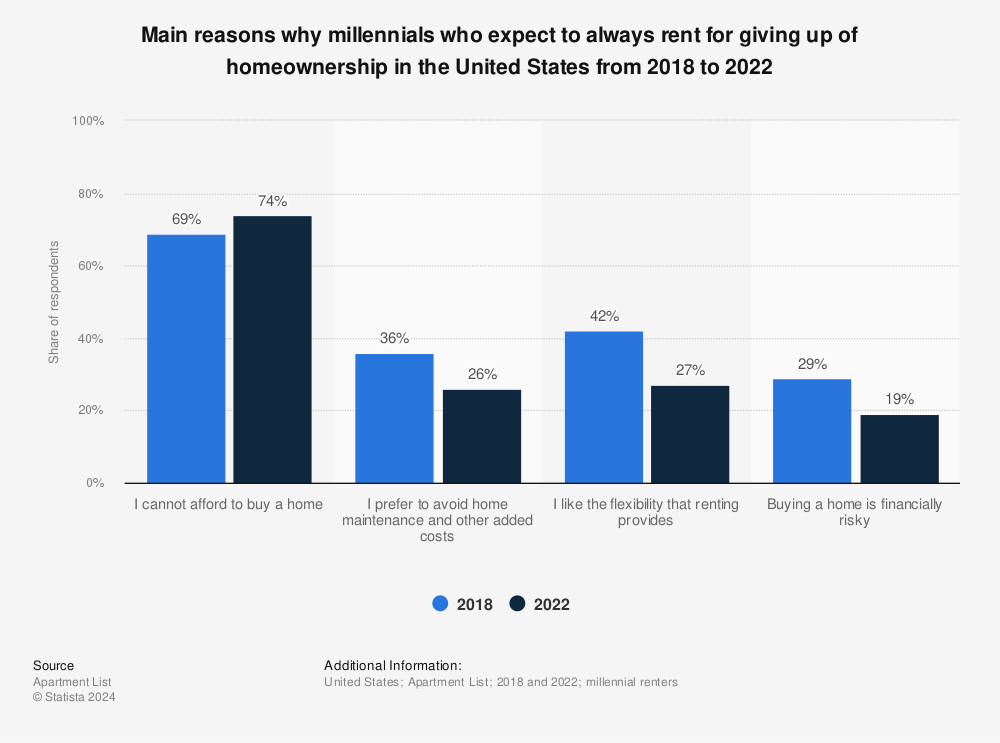

Why Aren’t Millennials Buying Homes?

Find more statistics at Statista

Millennials have different lifestyle preferences than older generations, often opting to rent a trendy downtown apartment rather than anchor themselves to a big house in the suburbs.

Others fall into the stereotype of living with their parents (often in the basement of one of those big suburban homes) through their twenties and into their thirties. Many choose to put off marriage and children, which are typically major factors in buying a first home, for several reasons.

“For older generations, success may have looked like a single family home, two kids, a comfortable retirement plan, and the annual family vacation. Many of today’s young people are spending their 20s and 30s traveling the world, going to happy hours, and posting on Instagram. They’re getting married and starting families later (if at all). They want freedom, in the workplace and in their lives.”

John Boitnott

As Americans, we value freedom. But millennials need to understand the trade-off they are embracing in an economy where home ownership is one of the middle class’s most important sources of long-term wealth. These lifestyle choices have repercussions not just for millennials personally but for the economy as a whole.

Millennial Home Ownership Is Impacted By Finances

Main reasons why Millennials who expect to always rent for giving up of homeownership in the United States from 2020 to 2021

The other major factor limiting millennial homeownership is finances. According to CNBC, nearly half of millennials who rent pay more than 30 percent of their income.

Combine that with stagnant wages and student debt, and it’s next to impossible to save up the kind of down payment that makes buying a home a viable option. And as aging baby boomers begin to sell their houses, the current homebuyers will likely be unable to afford them.

Obviously, there will be many changes in the U.S. housing market (and the economy in general) in the coming decades. The Urban Institute suggests changes to the mortgage process and zoning laws to promote greater millennial home ownership, but their major suggestions center around education.

Millennials tend to be ignorant about finances in general and have misconceptions about buying a home.

What You Don’t Know Can Hurt You

We say it a lot around here, but the most important thing you can do for your personal finances is to keep learning. Understanding our economic system is a great place to start.

Think about where you want to be ten, twenty, or thirty years from now, and start planning to get there. Even if your goals change in the meantime, achieving more financial stability now will never be a bad thing.